HOME | QUICK START | IN DEPTH | ABOUT ME | ABOUT APP

In Depth Tutorial on Using GridTracks

Finalizing the General Journal and General Ledger

Every once in a while, you will want to check your General Journal and General Ledger for any errors in inputing that might pop-up. While GridTracks ensures that all transactions entered are balanced, meaning that the amount debited into accounts must equal the amount credited into accounts, you do need to make sure that the Starting Values of the accounts are balanced, otherwise nothing will be balanced.

Balancing Starting Values

Note that because you can start using GridTracks to do your finances whenever you want to, you can set a starting value for all accounts. For example, if your bank account already has a balance of $5,000.00, it does not make sense to create a transaction for it as no transaction has occurred. Thus, you would want to assign the bank account starting value to $5,000.00.

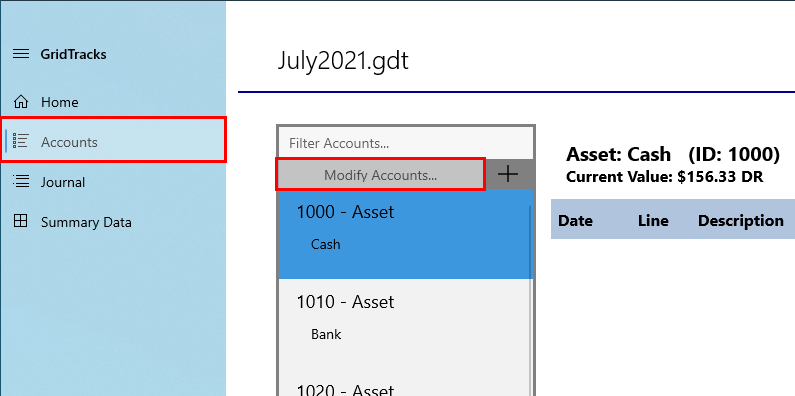

While GridTracks will not produce an error if the starting values are not balanced, if you go to the "Modify Accounts…" page, at the bottom you will see:

Note that when you open GridTracks, go to the Accounts page on the navigation pane on the left, and from there hit Modify Accounts…. This will take you to the page below, where you see a bird-eye's view of all the accounts in your General Ledger. At the very bottom, you will see Starting Value Quantities. Note that you are presented with total Debit balance (DR), total Credit balance (CR), and the difference between the two. Note that if the Difference is a DR balance, you will need to add more Credits to the starting values to get this quantity down to $0.00. As such, if the difference is a CR balance, you would need to add more Debits to the starting value to get the quantity down to $0.00.

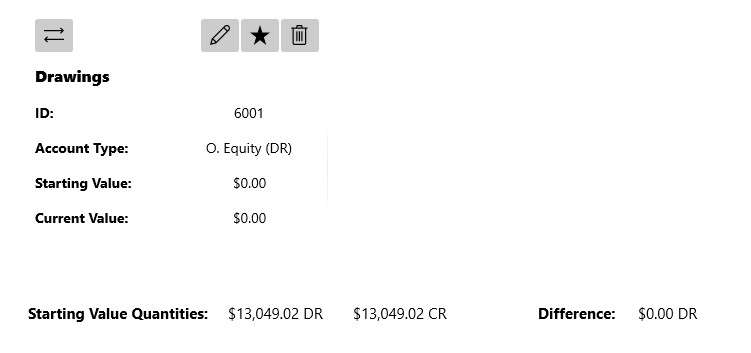

Note: GridTracks will allow you to delete an account with a non-zero starting balance, provided that it does not have any account entry posts in it. This means that if you do delete an account, you should come back to this "Modify Accounts…" page to double check that the Difference is still $0.00.

Double-Checking Entry Data

When you go through the process of double-checking the data, you will want to take a "snapshot" of your document. This can be as making a copy of the file in File Explorer on Windows. Alternatively, you can use Save As... in GridTracks, but be sure to reopen the original file again, because if you do not you will be running edits on the duplicate instead of the original.

In general, you want to first start with checking your Cash and Bank assets. As most transactions involve money, whether you are buying, selling, spending, or earning. Here are a couple of things to look out for when reconciling:

-

Credit Card Fees

When your customers pay with credit cards, this goes directly to your cash or Bank. However, you need to account for credit card fees from the transaction, as this will lower the amount of money you get. Below is a list of credit card fees to consider:

-

Address Verification Service Fee

When you business accepts purchases online or through the phone, this is the fee you have to pay to the bank to verify that the credit card is not fraudulent. Note that the fee is per transaction.

-

Discount Rate

If your business accepts credit card, you must pay a Discount Rate fee, based on a percentage of sale or return transactions. This percentage can vary by type of business and number of sales. If you accept credit cards electronically, you will probably pay lower fees because it is less work for the bank.

-

Secure Payment Gateway Fee

For online businesses—a fee that make sure that the transaction is occuring securely. The fee will be a fixed monthly amount.

-

Customer Support Fee

If you need to process credit card transactions 24/7, all year, then you will have to pay an additional fee to cover this. This is ideal for online businesses, where the customer can order at any time he/she pleases.

-

Monthly Minimum Fee

A monthly fee you will have pay for the privilege of accepting credit cards. This fee must be paid even if you make no credit card sales during the month.

-

Transaction Fee

A fee you must pay per transaction for every debit and credit card submitted for authorization. Even if the card is declined, you must still pay this fee.

-

Equipment and Software Fees

A fee for buying/renting the equipment and software required to accept credit and debit cards.

-

Chargeback and Retrieval Fees

A fee if the customer contests the transaction.

In order to properly reconcile payments through credit card, double check all of your business's transactions for the month, the amount of transactions paid with credit cards, and the fees associated with them. Once you have done this, you can apply the values to a credit card expense account. Note that all credit card expenses are lumped in the expense account Credit Card Fees Expense.

Here is an example where you are paying for credit card fees with cash

Date Post Debit Credit Sept 16 Credit Card Fees Expense (5880) 150.00 Cash (1000) 150.00 Paid credit card fees for the month. Please note that if the customer disputes the charge, you must first undo the sale:

Here is an example where you are paying for credit card fees with cash:

Date Post Debit Credit Sept 16 Sales (4225) 200.00 Cash (1000) 200.00 Customer disputed purchase of mixer. You can just undo this transaction when the issue is resolved and you get the money from the purchase:

Date Post Debit Credit Sept 16 Cash (1000) 200.00 Sales (4225) 200.00 Customer dispute for sale of mixer resolved. -

Address Verification Service Fee

Reconciling Your Bank Accounts

GridTracks makes it very easy to reconcile your bank accounts. In order to start this, go to your bank accounts to get a list of transactions made for the period you are interested in (monthly, every 3 months, yearly, or as such).

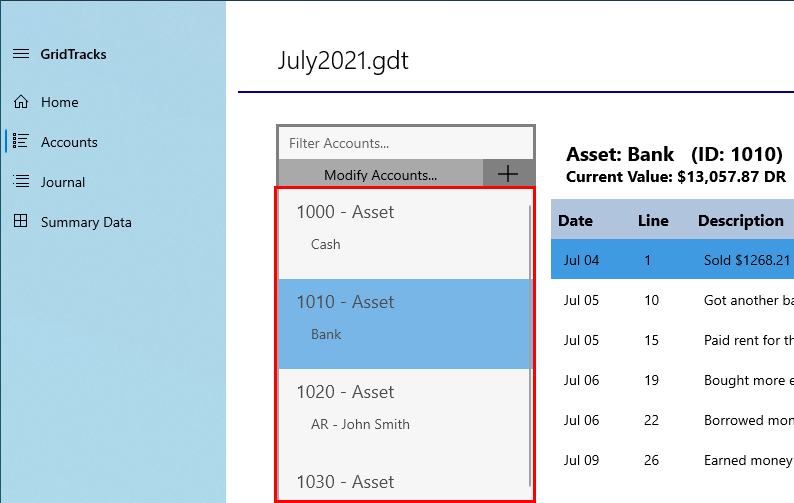

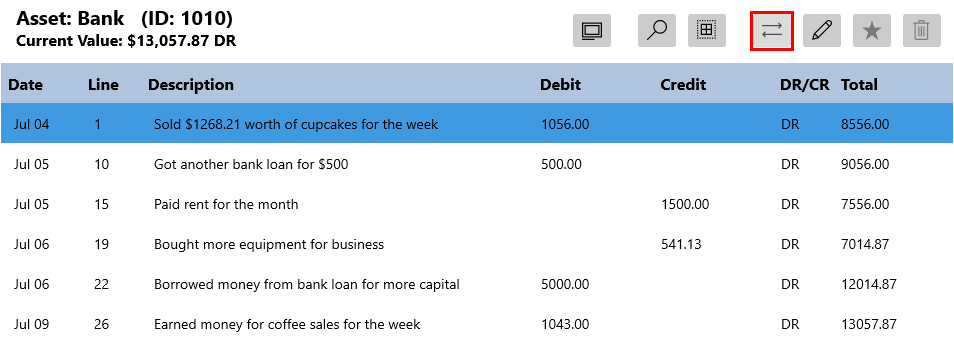

To start the reconciliation process, first go to your General Ledger in GridTracks, by clicking on the Accounts page in the navigation view on the lefthand side. Once you are in, you can access the information of any account you please. Hit "1010 — Asset (Bank)" to view the bank account:

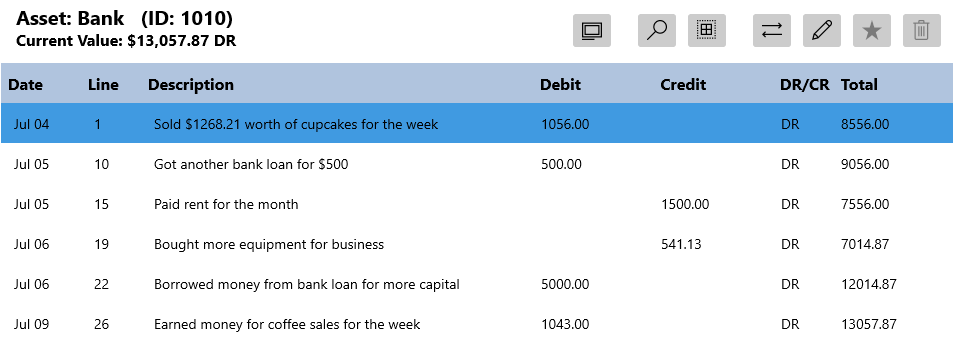

Here you can match up transaction from your bank statement to the ones in GridTracks.

Note that any debit posts would be considered "deposits", while credit posts would be money spent. Note that the total on the very right represents your bank balance. If the DR/CR column says DR, that means that your bank balance is debit valued and thus positive. If it states CR, then your bank balance is credit valued and thus negative. Please take warning if it is a CR balance, as this means you may have to pay overdraft fees for having a negative balance. GridTracks will highlight any account entries in red if they have a negative balance.

Sometimes, there may be cases where the order of which transactions taken place in your GridTracks document do not appear in the same order than in your bank statement. While this will not impact the accuracy of your finances, you may prefer for the numbers to line up. As GridTracks only sorts transactions by date, transactions of the same date are posted in an arbitrary order. In order to adjust a transaction, you need to hit the Toggle to Journal button highlighted in red below:

Note that this will take you to the Journal page, where you can move the transaction up or down from there. You can of course toggle from the Journal back to the Accounts page by hitting Go to Account….

You can only move transactions up or down if the transaction preceding it or succeeding it has the same transaction date, respectively.

Finally, if you do have bank errors, it is best to speak with your bank as soon as possible.

Accounts Receivable and Accounts Payable

To ensure accuracy in reconciliation of Accounts Receivable and Accounts Payable, it is helpful to use an Aging Summary. This summary goes over what has been paid in Accounts Receivable and what is upcoming.

For Accounts Receivable, the table would look like:

| Customer | Current | 31-60 days | 61-90 days | > 90 days |

|---|---|---|---|---|

| J. Smith | $500.00 | $250.00 | - | - |

| E. Fay | $275.00 | $250.00 | $100.00 | - |

| B. Johns | $600.00 | $175.00 | - | - |

| R. Ray | $550.00 | $250.00 | $50.00 | - |

| Total | $1925.00 | $925.00 | $150.00 | - |

Note that in the case of the example, the total amount in Accounts Receivable is ($1925.00 + $925.00 + $150 = $3,000.00).

Finally, if the customer has not paid after 90 days you may need to consider writing off the sale.

Just like with Accounts Receivable, you should make an aging summary with Accounts Payable, to make sure that the reconciliation matches up.

For Accounts Payable:

| Vendor | Current | 31-60 days | 61-90 days | > 90 days |

|---|---|---|---|---|

| Stock Foods Inc. | $485.00 | $265.00 | $100.00 | - |

| Mechanics 101 | $1,505.00 | $750.00 | $250.00 | - |

| Paper-Paper Ltd. | $600.00 | $175.00 | - | - |

| Furniture Fixture Co. | $750.00 | $300.00 | $150.00 | - |

| Total | $3,340.00 | $1,490.00 | $500.00 | - |

Note here that the total for Accounts Payable will be ($3,340.00 + $1,490.00 + $500.00 = $5330.00), and you total Accounts Payable in your books should reflect that.

Please be sure to use the Aging Summary to see what vendors need to be paid, as if you delay for too long it is possible your vendors will not let you buy products/services on credit. Because you need your vendors in order to create your goods/services, be careful.

Adjusting the Books

Asset Depreciation

Every month or so you should depreciate your assets, so that the expense of depreciation does not hit all at once, if you do monthly financial statemenbts. If you only make financial statements every year, then it is okay to only perform asset depreciation once per year. For more information on depreciation, go to the Asset Depreciation section of this guide.

Prepaid Insurance

Some insurance companies may make you pay for an insurance policy all at once for a large periods of time. For example, you may be required to pay $12,000 for car insurance at the beginning of the year, even though you will be using it for the whole year. If you were to expense this all at once, then all of the sudden your financial statements for the month will look horrendous. Thus, it is a better idea to keep an asset account called Prepaid Insurance, which stores the money you need to pay for insurance for the year. Each month, you would take the appropriate amount to apply to insurance expenses. Finally, because Prepaid Insurance is an asset, it will not show up in your income statement as a huge deficit.

If your business pays for insurance using your bank account, the transcation would look like:

| Date | Post | Debit | Credit |

|---|---|---|---|

| Oct 15 | Prepaid Insurance (1244) | 12,000.00 | |

| Bank (1010) | 12,000.00 | ||

| Allocated money from Bank to Prepaid Insurance. |

Then every month, you would pay the appropriate amount from Prepaid Insurance:

| Date | Post | Debit | Credit |

|---|---|---|---|

| Nov 15 | Vehicles Insurance (5884) | 1,000.00 | |

| Prepaid Insurance (1244) | 1,000.00 | ||

| Paid off vehicles insurance for Oct 15 to Nov 15. |

Note here that the monthly payment is $1,000, which is 1/12 the total amount paid for the year ($12,000.00).

Counting Inventory

It is possible at any time that you have made a mistake on the exact amount of inventory you have left when preparing your financial statements. Before every financial statement, make sure that the inventory stated in GridTracks matches that the actual count. Please go to Inventory and Sales for more info.

Bad Debts

As a business, it is inevitable that there may be some bad purchases, of which you never get paid for your good/service. It is ideal to account for this risk at the time of sale, because otherwise you will overestimate your assets. Note that this risk is accounted in the transaction below:

| Date | Post | Debit | Credit |

|---|---|---|---|

| Aug 22 | Bad Debt Expense (5900) | 1,000.00 | |

| Allowance for Doubtful Accounts (1900) | 1,000.00 | ||

| Believe that $1000.00 won't be paid back from Accounts Receivable. |

Note that the amount from Allowance for Doubtful Accounts matches up with Bad Debt Expense, as Allowance for Doubtful Accounts is a contra-asset that decreases the debit value of Accounts Receivable.

Write-offs for Bad Debt Expense can be found by:

-

By customer

By studying the required payments of individual customers on Accounts Receivable, you can determine which portions of the purchases on credit will need to be written-off.

-

Percentage of all Accounts Receivable

If your business has a good idea of the percentage of bad Accounts Receivable debts, you can directly compute the amount to put in Allowances for Doubtful Accounts.

-

By Percentage of Sales

Instead of writing-off a percentage of total Accounts Receivable, look at percentage of sales to see how much should be written-off. The consensus here is that the more products/services you sell, the more bad debt you will encounter.

Once every accounting period, as meantioned later, all revenue, expenses, and owner's equity (DR) are consolidated into Owner's Equity (CR), and all these accounts will then have a balance of zero. This means that while Bad Debt Expense will be reset to $0.00, the value for Allowance for Doubtful Accounts will remain at its current value.

Also, at the end of the accounting period, it is obvious that you will either overestimate or underestimate the amount you put in Bad Debt Expense and Allowance for Doubtful Accounts.

If you underestimate the amount put into Allowance for Doubtful Accounts, of which more money supposed to be written-off, you can always debit Bad Debt expense more.

| Date | Post | Debit | Credit |

|---|---|---|---|

| Nov 15 | Bad Debt Expense (5198) | 200.00 | |

| Allowance for Doubtful Accounts (1900) | 100.00 | ||

| Accounts Receivable—J. Smith (1200) | 300.00 | ||

| Wrote off purchase from J. Smith. |

Note here that there was not enough money in Allowance for Doubtful Accounts to write-off the full amount and thus an additional $200.00 was written-off.

If you have overestimated the amount you needed to write off, meaning there is some Allowance for Doubtful Accounts leftover, then you can just carry over this value for the next accounting period, and just put less money into Allowance for Doubtful Accounts to get to the amount you desire. If you wish, you could also credit (decrease) Bad Debt Expense and debit (decrease) Allowance for Doubtful Accounts such that Allowance for Doubtful Accounts is equal to zero.

Note that writing off a customer using Allowances for Doubtful Accounts, and if they end up paying in the end, can be found at the bottom of the Inventory and Sales page.

Unpaid Salaries and Wages

For the most part, if you pay wages weekly or bi-weekly, it is possible that the pay date may not be the same as the day that you provide your financial statements. For instance, if you paid your employees on March 15th, and your financial statement was made March 18th (assuming weekly pay), then there is three days worth of pay not accounted for.

Thus, in order to get an accurate breakdown of expenses, you must log in the salary/wages expense for those three days, even if you are not paying your employees again until March 22. As you cannot take the money out of cash (as you have not paid them cash yet), you would temoparily put it into a liability account called Accured Wages Payable.

If the amount of unpaid wages from March 15-18 is $2,500.00, then:

| Date | Post | Debit | Credit |

|---|---|---|---|

| Mar 18 | Wages and Salaries Expense (5500) | 2,500.00 | |

| Accured Wages Payable (2146) | 2,500.00 | ||

| Logged in wages for days March 15 to March 18, which have not been paid yet for. |

When it comes to the next period, you would convert the amount owed from Accured Wages Payable into your payment method for the employee, along with the rest of the wages owed (in case above, the wages from March 18 to March 22). Note that Wages and Salaries Expense shows up again to represent the payment amount from March 18 to March 22. In the example below, that is equal to $5,000.00. Also, the employee below is being paid from Bank.

| Date | Post | Debit | Credit |

|---|---|---|---|

| Mar 22 | Wages and Salaries Expense (5500) | 5,000.00 | |

| Accured Wages Payable (2146) | 2,500.00 | ||

| Bank (1010) | 7,500.00 | ||

| Paid employees for period from March 15 to March 22. |

Accured Unpaid Services

Just like in the case above for Unpaid Wages, it is also to have services that you have used partially that you have not paid for yet. For example, if you ordered repairs for a whole week, but you have to prepare a financial statement in the middle of the week, you must expense the portion of that work. This can be done simply with an Accounts Payable liability account, showing that you acknowledge you owe the money once you apply the expense.

Say that you calculated that the work from 3 days out of the week required is worth $1,000.00. This would be logged in as:

| Date | Post | Debit | Credit |

|---|---|---|---|

| Mar 22 | Improvements Expense (5541) | 1,000.00 | |

| Accounts Payable (2466) | 1,000.00 | ||

| Allocated money to pay for a portion of the work done this week. |

Accuring for Unpaid Interest

For instance, if you are only required to pay interest on a loan every three months, but make financial statements every month, then you will need to divide the amount up into thirds, so that the amount of expenses paid is evenly distributed (so that it does not look like one bad month and two goods ones). Just like in the case of unpaid wages and unpaid services, you would create a payable liability account that stores the amount you owe but have not paid for yet.

In the case below, the amount owed for interest for the month is $300.00.

| Date | Post | Debit | Credit |

|---|---|---|---|

| Mar 22 | Interest Expense (5244) | 300.00 | |

| Interest Payable (2566) | 300.00 | ||

| Created liability for paying of interest on bank loan. |

Note that once the three months are up, you would debit the Interest Payable liability (getting rid of it), and credit anotjer asset or liability account (decreasing what you own).

Accuring for Revenue

Just like in the cases above, you should also accrue for revenue that is unpaid yet. This is because work may have already began but not yet finished when making a financial statement, of which the amount done should be logged in as revenue. As this is like putting the work done on the customer's credit, you would charge the partial revenue into Accounts Receivable:

| Date | Post | Debit | Credit |

|---|---|---|---|

| Mar 22 | Accounts Receivable (5244) | 500.00 | |

| Service Revenue (2566) | 500.00 | ||

| Logged in revenue for the three days of work already done on the project. |

Adjusting for Unearned Revenue

As previously discussed in Inventory and Sales, it is possible that the customer may have either given you a deposit or have paid you directly before the service has started. In either case, you been given money or an Accounts Receivable, but no work has been done. As shown there, you would first record it in a Liability account called Unearned Revenue, as you have not technically earned the money yet.

| Date | Post | Debit | Credit |

|---|---|---|---|

| Mar 22 | Bank (1010) | 2,500.00 | |

| Unearned Revenue (2676) | 2,500.00 | ||

| Received total payment at beginning of the project. |

At the creation of the financial statements, you must decide, based on the amount of work done, how much of the Unearned Revenue liability will be converted into Service Revenue. For example, if the customer paid you $2,500.00 for a 2 month project, and by the time you are preparing the financial statement 1 month has elapsed, you would convert $1,250.00 worth of liability into service revenue.

| Date | Post | Debit | Credit |

|---|---|---|---|

| Apr 10 | Unearned Revenue (2676) | 1,250.00 | |

| Service Revenue (4089) | 1,250.00 | ||

| Finished half the project for J. Smith. |

Note that here we are debited the liability account, decreasing what we owe. Furthermore, crediting the revenue account means money has entered the system, as we would expect.

Transferring Revenue and Expenses

Finally, there might be times when you want to move expenses from one account to another, or revenue as well. This is commonly done when you want to keep track of a more specific expense or revenue, or when you wish to conslidate two or more expenses or revenues.

In the first case, you want to keep track of a more specific expense. For example, you may have noticed that paper seems to be taking a huge chunk of your Supplies Expense and you believe that it is possible your employees are being wasteful. In this case, you may want to separate paper expense from Supplies Expense, so you have a better idea of how much money is going towards it.

In the second case, there may be a time when you may also decide that it is no longer necessary to have to distinguish between two separate accounts and would like to merge the two. For example, in the future you switch to using tablets and paper is no longer an expense that shows up frequently. In that scenario, you may want to move the balance in Paper Expense back into Supplies Expense, and get rid of Paper Expense. Note that GridTracks does not allow the deletion of accounts with account entry posts, however, you can deprecate an account. When an account is deprecated, you can no longer create transactions using it, and when you complete your books and start over, the account will not be passed on.

In either case, transferring amounts from revenue-to-revenue, or from expense-to-expense is fairly simple. Just remember that crediting a revenue is what increases it, while debiting a revenue decreases it. Thus, credit the revenue account you wish to add to, and debit the revenue account you wish to remove from. Do the same for expenses but in reverse, as expense accounts increase when debited and decrease when credited.

From the example above:

| Date | Post | Debit | Credit |

|---|---|---|---|

| Apr 10 | Paper Expense (5441) | 175.00 | |

| Supplies Expense (5436) | 175.00 | ||

| Separated Paper Expenses from supplies for better tracking. |

For Revenue accounts, the transaction would look similar. Below, we are separating Advertising Revenue from Other Revenue, as we want a better picture:

| Date | Post | Debit | Credit |

|---|---|---|---|

| Apr 10 | Other Revenue (4115) | 500.00 | |

| Advertising Revenue (4536) | 500.00 | ||

| Separated Advertising Revenue from general Other Revenue for better tracking. |

Next Steps

Credits

Please note that most of the information from this site is taken from the book "Bookkeeping for Canadians for dummies" by Lita Epstein and Cécile Laurin.

(Epstein, L., & Laurin, C. (2019). Bookkeeping For Canadians For Dummies. Hoboken, New Jersey: John Wiley & Sons, Inc.)