Basics of Creating Accounts

Before you begin with keeping track of your transactions, it is important to first decide what accounts you wish to keep track of. There must be enough accounts

to record each transaction you make. By virtue of making these accounts, you can see how the balance in these accounts change due to the logging in of journal

transactions.

As mentioned in Introduction, there are six types of accounts: assets, liabilities, revenues, expenses, owner's equity (DR), and owner's equity (CR).

Again, assets are what you own and liabilties are what you owe. Revenue is when you profit and money enters your business. Expenses are bills you have to pay,

causing money to leave your business. Finally, owner's equity (DR) represents accounts of both drawings and dividends, which is when the owner or shareholder

takes money out of the business for personal reasons. Of course, by virtue owner's equity (CR) represents the net worth of the business.

In GridTracks, all accounts must have both an account ID and an account name, as well as an account type as listed above. It is optional to assign a starting value

to an account. Typically, your accounts will have a starting balanace before any transactions are applied,and this would be the place to input them. Please ensure

that the debit balances and credit balances of the starting values must be balanced as well. As all journal transactions must also be balanced, unbalanced starting

values cannot be corrected, which is why balancing is so important.

Note that GridTracks will only accept account IDs between 1 and 9999 inclusive. Because GridTracks sorts accounts by their account ID, it is important to pick your

IDs accordingly. Below are the typically ranges per account type, but you can obviously pick to your discretion.

| Account Type |

Suggested Account ID Range |

| Asset |

1000-1999 |

| Liability |

2000-2999 |

| Owner's Equity (CR) |

3000-3999 |

| Revenue |

4000-4999 |

| Expense |

5000-5999 |

| Owner's Equity (DR) |

6000-6999 |

When you are making your accounts, please space out your account IDs by at least 10 unit incrememts. What I mean is do not create account IDs 1000, 1001, 1002, etc., and

instead, try 1000, 1010, 1020, 1030, etc. This is because GridTracks orders accounts by their ID, so if you want to squeeze a new account between two existing (like ID 1005,

which is between 1000 and 1010), you won't have to renumber all subsequent accounts after.

Adding/Editing Accounts in GridTracks

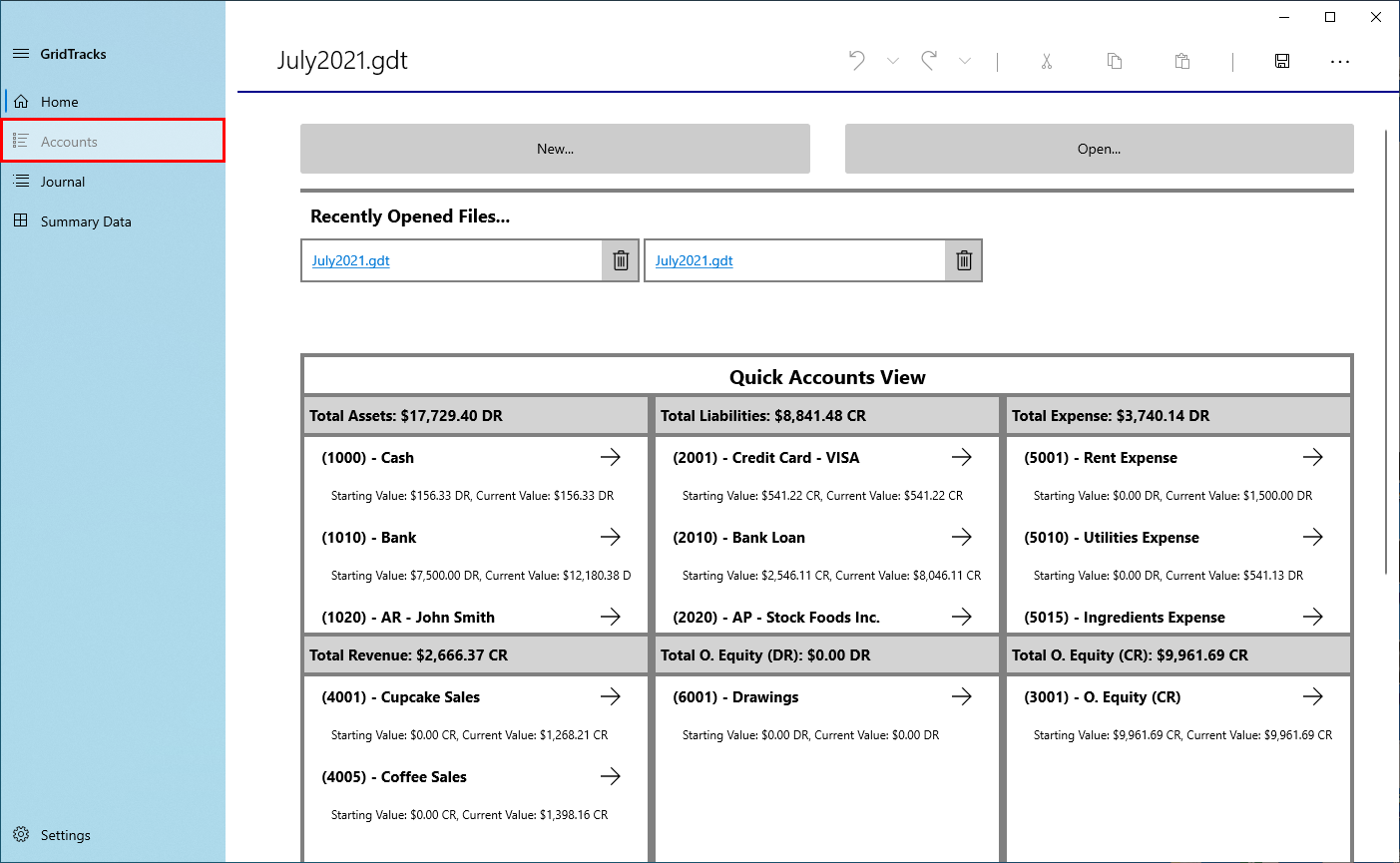

When you start GridTracks, you are greeted with this Welcome page. Note that here I have a file opened titled July2021.gdt.

Click on the area highlighted to go to the Accounts page, where you can begin adding/editing accounts. You will be taken to the page below:

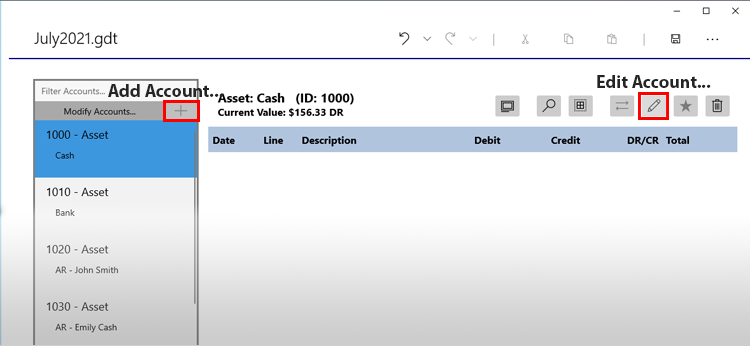

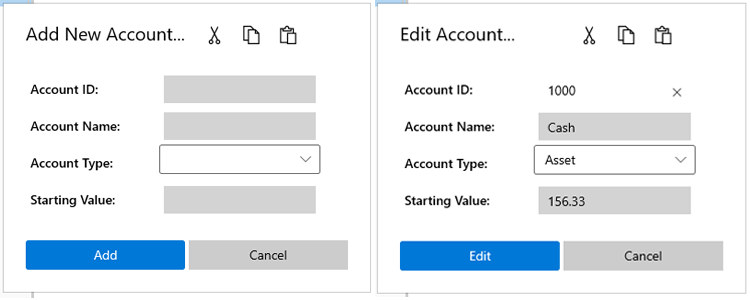

Notice highighted in red the "Add Account..." and "Edit Account...". Either will open the respective dialog boxes below:

The only difference between the two is the title of the dialog, as well as the fact that GridTracks will fill in the boxes depending on saved account data.

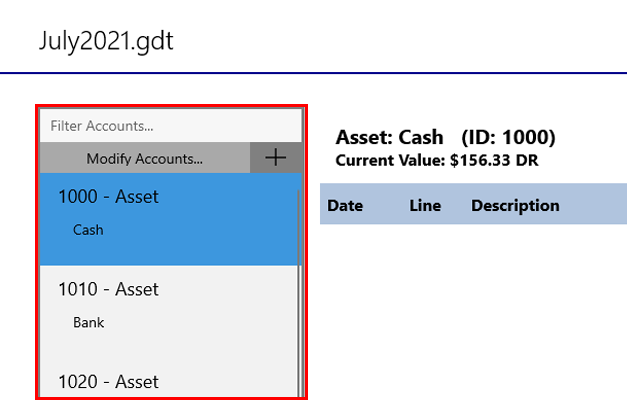

On the left side of the Accounts page, notice the pane. Here, there is a list of all accounts in your document. Clicking one will make it the active account, and the

pane on the right will show all account entries of that account (account entries, which come from journal transactions, will be discussed later). Hitting the Edit Accounts

button will only edit the active account.

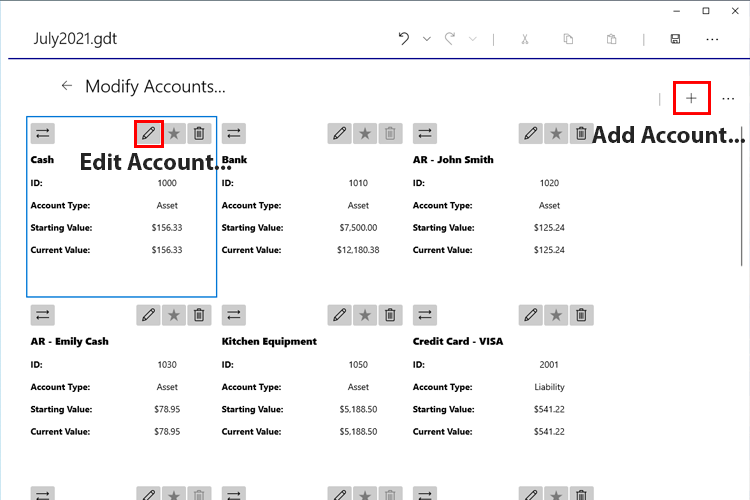

Furthermore, the Filter Box will allow you to text-filter what accounts you wish to see in the list of accounts. Finally, clicking the "Modify Accounts…"

button will take you to the page below:

Here, you can also add/edit accounts as well, with more of a bird eye's view. I recommend this mode for when you need to multiple accounts at a time, as it shows

the account ID, name, starting value, type, and current value of all accounts at once.

What Accounts Should I Add?

Note that the table below discusses the various types of accounts you can create for your GridTracks document. Please feel free to pick and choose whichever accounts are best

for your own business.

Note that most of the accounts are their descriptions were inspired by the book "Bookeeping for Canadians for Dummies" by Lita Epstein and Cécile Laurin.

(Epstein, L., & Laurin, C. (2019). Bookkeeping For Canadians For Dummies. Hoboken, New Jersey: John Wiley & Sons, Inc.)

| Account Type |

Possible Accounts to Add |

| Assets |

Assets can be broken down into Current Assets, as well as Long Term Assets. Current assets are those that you will use

within 12 months, while Long Term Assets are those that are there fort longer than 12 months.

Current Assets

-

Cash in Chequing

This represents the amount of cash in your bank chequing account.

-

Cash in Savings

This is the amount of cash in your bank savings account.

-

Cash on Hand

This is any cash in your business that you have on hand and not in a bank account. For example, cash in registers at a retail store would fall under this

category.

-

Accounts Receivable

This is to keep track of payments from customers that have paid using credit. Note that credit cards do not fall under this category

because you are paid immediately from the bank. These can be labeled as "AR — [Customer Name]".

-

Inventory

Here you can keep track of the dollar amount of the inventory you currently have on hand.

-

Prepaid Insurance

This is money set aside to pay for insurance. Money is taken out of this balance when paying for insurance.

Long Term Assets

-

Land

This asset is reserved for the price of the land purchased. Note that this does not include the building itself, because

land does not depreciate, but the building on it does.

-

Buildings

Use this asset to keep track of the value of the buildings on your land for your business. Note that this asset undergoes asset depreciation.

-

Leasehold Improvements

This asset represents upgrades to a leased property. For example, when running a business in a shopping mall, it normally comes as an empty

room, and you must spend capital to furnish it. This asset also undergoes asset depreciation.

-

Vehicles

This asset represents any vehicles (e.g. cars, trucks, etc.) that are bought by the business. If the vehicles have any improvements to them,

include that in the value applied to this asset. The Vehicles asset undergoes asset depreciation as well.

-

Furniture and Fixtures

This asset represents all furniture and fixtures, including chairs, desks, shelves, and such. This asset also undergoes asset depreciation.

-

Equipment

This asset represents all equipment that is kept for over a year. This can include computers, copy machines, and other equipment required

for your business to run smoothly. This asset also undergoes asset depreciation.

-

Accumulated Depreciation

This family of assets is used to keep track of the depreciation value of assets that undergo asset depreciation. It is ideal to have multiple

"Accumulated Depreciation" accounts, each titled "A. Depreciation — [Asset Account]". Asset depreciation will be discussed in more

detail later on.

-

Patents

This represents the amount of money the business has spent on gaining specific patents. Note that because patents are only valid for a certain period of time,

they undergo amortization (which is depreciation for intangible assets).

-

Copyrights

This represents the amount of money required to establish copyrights. As copyrights expire after a certain period of time, they also undergo

amortizaton.

-

Accumulated Amortization — Patents/Copyrights

This is where you record the depreciation of your patents/copyrights.

-

Goodwill

Only use this asset if you have purchased another business for over the market value of all that business' net assets. This account

is used to keep track of intangible assets owned by that business, such as store locations, business reputation, customer loyalty, and such.

If your asset does not fall into one of these categories, you can put in under a generic umbrella account such as "Other Assets", and move the asset to a

different asset account at a later date.

|

| Liabilities |

Note that liabilities can also be broken down into Current Liabilities and Long Term Liabilities, where again, current

liablities are those that are paid in the next 12 months, with long term liabilties going beyond that.

Current Liabilities

-

Accounts Payable

This liability represents money owed to vendors, contractors, and suppliers that are to paid within a year. Of course, the terms of this

liabilities depends on the terms of agreement made with the outside party. These set of accounts can be labeled as "AP — [Company Name]".

-

GST/Retail Taxes Payable

When you charge the Goods and Service Tax or other Retail Taxes, the amount that you charge is initially put into your bank account.

In order to show that this money is meant to go to paying taxes and is thus no owned by you per say, this account is needed (more on it when we look at journal

transactions).

-

Payroll Taxes

Same concept with GST/Retail Taxes, but with payroll taxes from employees.

-

Credit Cards Payable

You can keep multiple liability accounts for each credit card that you have. Note that credit cards should only be used for short term loans

due to their high interest rates, and thus long term loans should be transferred to lower interest bank loan.

Long Term Liabilities

-

Loans Payable

These set of liability accounts keeps track of all long term loans that will exist for longer than a year. This includes mortgages and vehicle loans.

-

Notes Payable

This is used when you borrow money from other businesses using promissory notes — this note contains terms for repayment as well as interest.

This type of loan does not require asset as collateral.

|

| Owner's Equity (CR) |

As mentioned early, Owner's Equity (CR) represents the equity of all shareholders/partners in the business. Accounts of this type include:

-

Common Shares

This account is only needed for corporations. It is used to keep track of the investors contributions to the business.

-

Retained Earnings

This equity account is also only needed for corporations. This account keeps track of all profits and losses accumulated since the business first opened, updated yearly.

-

Capital

This set of equity accounts is for unincorporated businesses — you need one account for each owner within the business. This set of

accounts allows you to keep track of who invested what into the business, whether it be cash, a vehicle, land, and any other such assets. Any profits or losses are

accumulated into the various Capital accounts after certain periods of time.

|

| Revenue/Income |

Revenue/Income represents a portion of your income statement. These are accounts that allow you to keep track of your profits over a certain

duration of time. Once that period has ended, net income/loss is consolidated into Retained Earnings/Capital equity accounts as mentioned above.

-

Sales and Service Revenue

This account keeps track of all profit from sales and services run by the business.

-

Other Income

This account keeps track of secondary profits for the business (income that would not fall under Sales and Service Revenue).

-

Interest Income

This account is for money earned from interest on a savings account, accounts receivable, a long-term loan, and such.

-

Rent Revenue

When your business rents out property to other businesses/persons, you would want to keep track of those profits here.

-

Gain on Disposal of Fixed Assets

If you sell a fixed asset, and you made a profit from the sale, it would go into this account. Note that the profit made must take the depreciation amount

into consideration.

-

Purchase Discount

Sometimes vendors will give you a discount on the purchase if you are able to pay them within a certain period of time. Any discounts of this manner go into

the purchase discount.

-

Purchase Returns and Allowances

When you are unhappy with a product purchased, the vendor may provide you with a reduction in purchase price to make up for it, or will allow you to return it.

In either case, be sure to log either the return price or the discount price in this account.

|

| Expenses |

Expenses are accounts that take money out of your assets to pay these accounts. Note that it is the combination of the amounts in both revenue adding

expenses that determines whether your business had a net income or loss. Note that Cost of Goods Sold falls under Expense accounts.

Cost of Sales Expenses

-

Sales Discounts

When you provide discounts for earlier payments, this account will hold that value as a cost to you.

-

Volume Discounts

This account holds discounts for large volume purchases or for fostering better relationships with customers. This account holds this value as cost to you.

-

Sales Returns and Allowances

When the customer returns an item or is given a discount for a defective item (of which they would in turn keep), the cost of this goes into this expense

account.

-

Purchases

This expense account is used to store the total cost of goods you wish to sell.

-

Freight-In Charges

This expense account is used to store the amount of money spent on shipping costs when purchasing products.

Other Expenses

-

Loss on Disposal of Fixed Assets

If you sell a fixed asset at a loss, then that amount would go into this account. Note that loss is dependent on the depreciated amount of the asset, much like with

Gain on Disposal of Fixed Assets mentioned above.

-

Advertising and Promotion

Any money spent on advertising and promotion, such as TV ads, Google ads, printing/distribution of flyers, and such, is kept track of in this account.

-

Automotive Expense

This expense account tracks money spent on the maintenance of vehicles.

-

Bank Service Charges

This account tracks the amount of money spent on bank fees (e.g. chequing account fees, E-transfer, etc.).

-

Depreciation and Amortization

A consolidated expense account that keeps tracks of all depreciation/amortization.

-

Dues and Subscriptions

An expense account for keeping track of all subscription services that your business uses.

-

Equipment Rental

The fees for any equipment that is rented for business purposes would fall under this expense account. For example, truck rental for the purpose of moving

business goods would fall under this category.

-

Interest

Any interest that arises from borrowed money would go under this expense account.

-

Insurance

Fees for insurance would fall under this set of expense accounts. Note that you should most likely make different insurance expense accounts for different things

(i.e. car insurance and home insurance would be different accounts).

-

Legal and Accounting

When the business pays for any legal or accounting services, those expensese fit in here.

-

Maintenance and Repairs

Anything used to maintain fixed assets or improvements to rental property would fall under this expense.

-

Miscellaneous Expenses

Use this expense account for when you have expenses that do not fall into any other category (use this account at your discretion).

-

Office Expense

Any supplies needed for the office to run smoothly, such as paper and pens, which do not fall under Fixed Assets would fall into this expense account.

If you wish to keep track of a specific office expense, such as pens, you can make a separate Office Expense account just for pens.

-

Payroll Benefits

Things like retirement benefits and employment insurance for workers would fall under this category.

-

Postage and Delivery

This set of accounts keeps track of the amount of money the business spends on delivery goods. You may wish to keep track of different delivery companies

to see where exactly you are spending your money. Note that this is different from Freight-In Charges, which only applies to the cost of shipping

in the process of purchasing goods to sell.

-

Rent Expense

Any expenses coming from the rental of property, such as rented office space or rented desks, fall into this category.

-

Salaries and Wages

Use this expense account to keep track of the wages you have paid your employees (it may be helpful to keep vacation pay in a different account).

-

Supplies Expense

Use this expense account for business specific supplies that do not fall under Office Expense.

-

Travel and Entertainment

Expenses that arise from employees needing to travel and for entertainment purposes (e.g. box seats at a basketball game) would be kept track of here.

-

Telephone and Internet

Use this expense account to keep track of money used to pay for telephone and internet.

-

Utilities

This expense account is used to keeping track of utilities such as water, heating, and electricty.

|

| Owner's Equity (DR) |

These accounts exist for when the owner or shareholder of the business takes money out (note that this money is not considered a salary).

-

Drawings

This set of accounts is only for unincorporated businesses, where each owner of the business needs their own account, to record

how much money is taken out of the business for personal reasons.

-

Dividends

This set of accounts is for incorporated businesses. It is the same as Drawings, but considering shareholders instead.

|

Please be advised that if the above table is overwhelming to you, do not stress as you can choose to add new accounts (or delete them) any time you choose.

Next Steps

Credits

Please note that most of the information from this site is taken from the book "Bookkeeping for Canadians for dummies" by Lita Epstein and Cécile Laurin.

(Epstein, L., & Laurin, C. (2019). Bookkeeping For Canadians For Dummies. Hoboken, New Jersey: John Wiley & Sons, Inc.)